Analysis

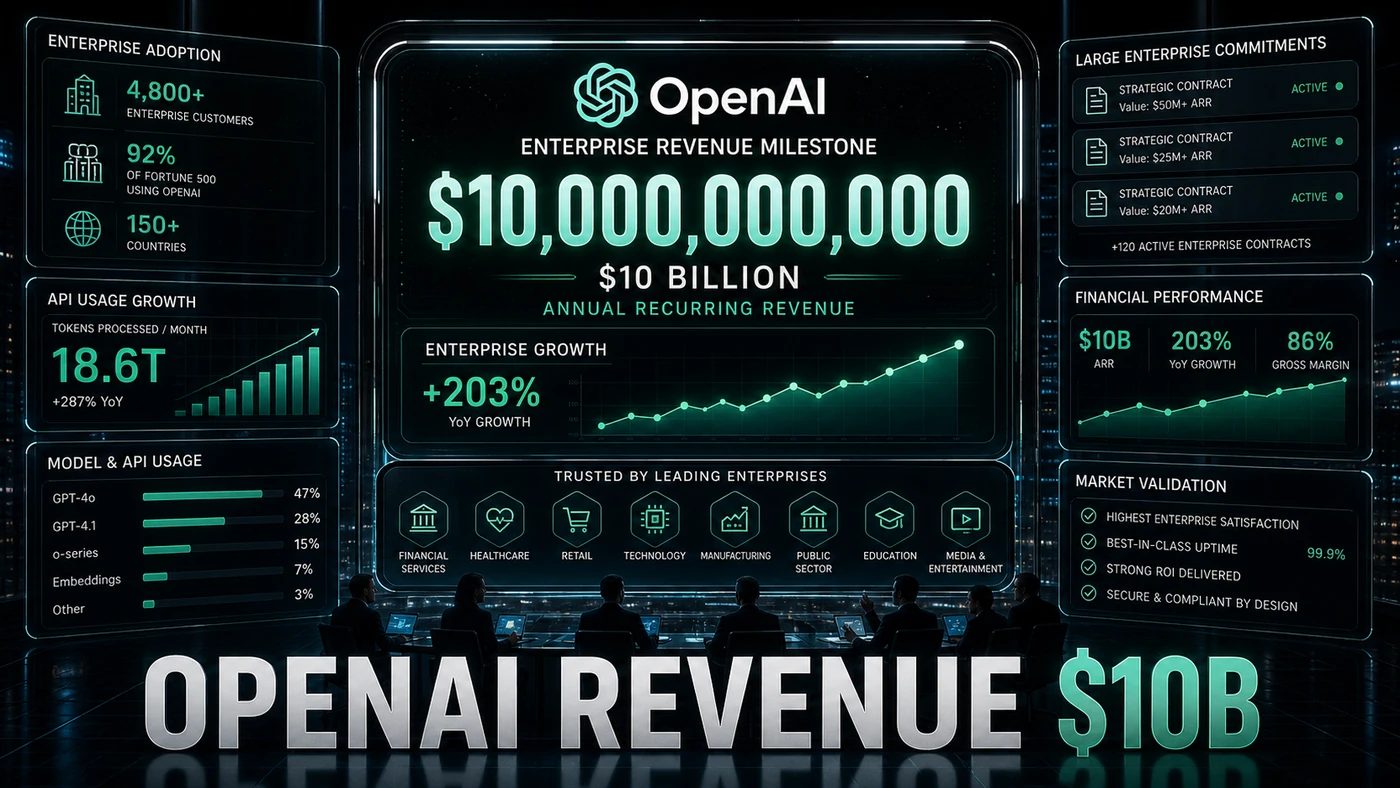

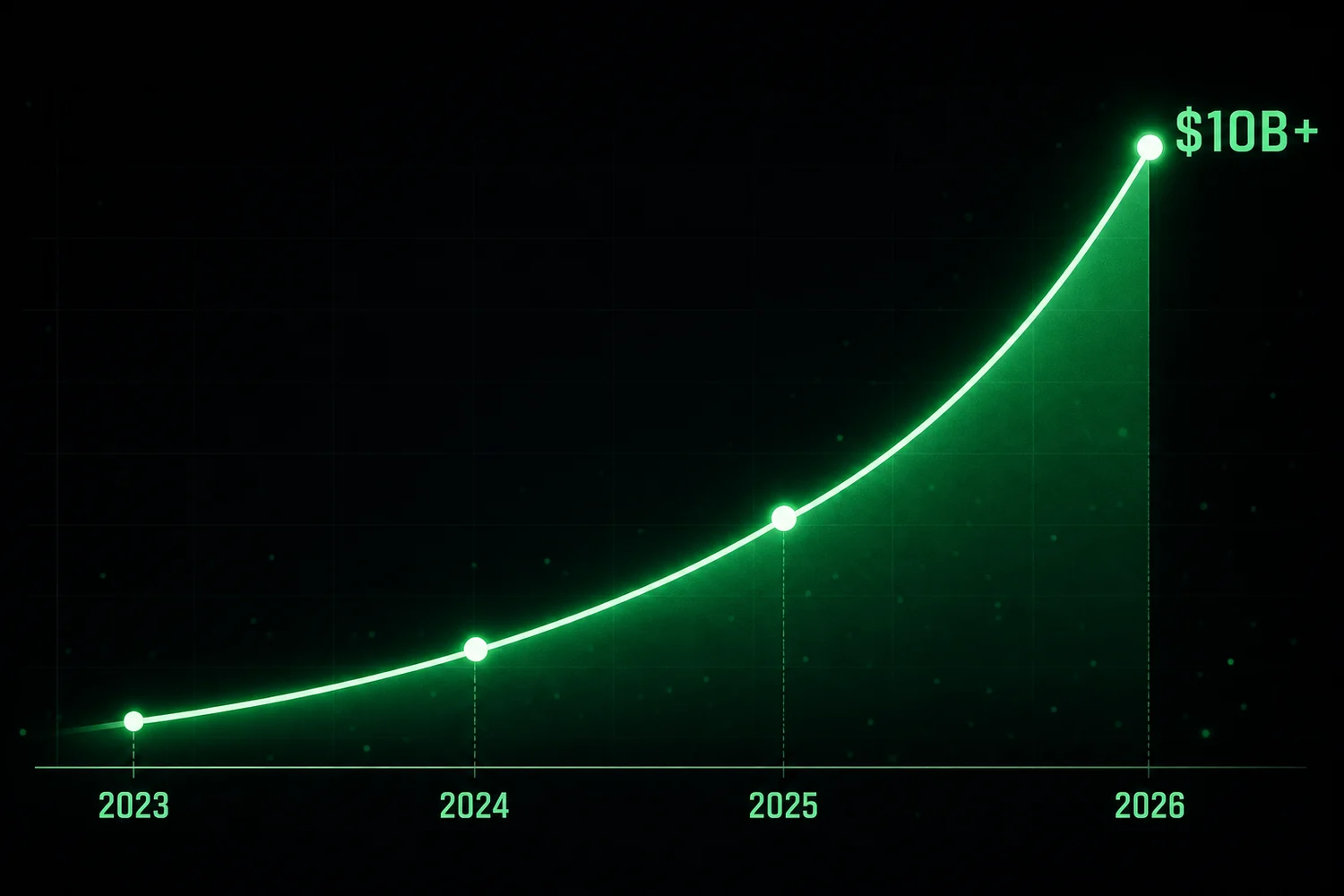

By any normal yardstick, going from a billion dollars to ten billion in annualised revenue takes a long time. OpenAI is reported to have done it on enterprise sales in under two years, with the $10 billion mark said to have been hit in May 2026. Treat the exact figure and date with caution: published sources put $10 billion as OpenAI's *total* run rate back in mid-2025, and have its overall revenue well past that by early 2026, so the precise "enterprise-only, May 2026" framing here is unconfirmed.

What is not in doubt is the direction. Big companies that spent 2024 running cautious pilots have moved real budget into AI, and OpenAI has captured a large share of it. That is the story under the number: how a vendor turned curiosity into signed contracts faster than almost anyone expected.

For an Australian business team watching from the sidelines, the "so what" is simple. The tools your competitors are trialling are no longer experiments, they are line items. The rest of this piece digs into what drove the growth, who is buying, and why the run may get harder from here.

In the history of enterprise software, few companies are said to have grown from $1 billion to $10 billion in annualised revenue this quickly, though no primary source confirms that exact enterprise-only trajectory (Yahoo Finance, OpenAI says enterprise AI is already 40% of revenue). The milestone, reported by sources familiar with the company's financials in May 2026, points to more than a vote of confidence in OpenAI's technology. It reflects a change in how businesses buy and run AI.

OpenAI's revenue comes from three places: ChatGPT Plus consumer subscriptions, ChatGPT Enterprise and Team subscriptions, and API usage. The $10 billion figure is said to cover enterprise revenue, Enterprise, Team, and API combined, and to exclude the consumer Plus business, which one estimate puts at an extra $2-3 billion a year. That Plus figure is unconfirmed, and other reporting suggests consumer is actually the larger share of total revenue (Yahoo Finance, enterprise ~40% of revenue).

The Enterprise Adoption Drivers

A few things pushed the growth along. The release of GPT-5.5 in April 2026 gave businesses a model reliable enough to put into production in regulated industries. Its 58.6% score on SWE-bench Pro, the harder real-world GitHub variant, not the easier Verified benchmark where it sits near 88.7%, does not top the market. But its consistency, its safety profile, and the maturity of OpenAI's enterprise tooling made it the safe default for organisations that hate surprises.

ChatGPT Enterprise also turned out to be a strong land-and-expand product. Companies tend to start small, a few hundred seats in one department, then add more as the use cases pile up. OpenAI is reported to say the average enterprise customer grows its seat count by 4.5x in the first year, though that figure is unconfirmed. Either way, the dynamic is what matters: revenue from existing customers keeps compounding while new ones come on board.

The API platform has grown up too. Fine-tuning infrastructure, built-in evaluation tools, and enterprise-grade certifications, SOC 2 Type II, a HIPAA Business Associate Agreement, and GDPR compliance, have cleared the hurdles that used to block production use. One caveat worth flagging: the Assistants API, which simplified building agent-style apps and was reportedly an adoption driver, has since been deprecated and is scheduled to shut down on 26 August 2026, with OpenAI steering developers to the Responses API. So that particular driver is no longer one to lean on.

Customer Composition

OpenAI's enterprise customers span every major industry. Financial services is reportedly the biggest vertical, at around 22% of enterprise revenue, on use cases like document analysis, compliance checking, and customer service automation. Healthcare is said to be the fastest-growing, with revenue up 340% year-over-year as organisations apply AI to clinical documentation, prior authorisation, and patient communication. OpenAI does not publish vertical revenue splits, so both the 22% share and the 340% figure are unconfirmed.

The company is reported to have over 1.2 million enterprise seats active globally across more than 15,000 organisations, and to have seen average contract value climb from $48,000 in early 2025 to over $185,000 by mid-2026, reflecting both seat growth and higher-value API work. None of these figures has a traceable primary source; treat them as company-reported estimates.

Competitive Positioning

If the $10 billion holds, it sits well ahead of OpenAI's nearest rivals, though most competitor revenue numbers here are analyst estimates rather than published figures. Anthropic's annualised revenue has been put at $1.8-2.2 billion, but that range looks low: mid-2026 reporting had Anthropic materially higher, and the Fable 5 suspension adds near-term uncertainty. Google's AI enterprise revenue, spanning Vertex AI and Workspace AI, has been estimated at $3-4 billion and growing fast. Microsoft's Copilot revenue is reportedly in the $5-6 billion range a year, though that figure isn't broken out publicly and includes plenty of non-OpenAI models.

The field is getting crowded. Google's Gemini 3.5 Flash offers comparable capability at lower prices with tight Google Cloud integration. Anthropic's Opus 4.8 leads on several benchmarks and has a foothold in safety-conscious industries. And the open-weights wave, MiniMax M3, GLM-5.2, Llama 4, gives businesses a route that drops vendor lock-in and API bills entirely.

The Sustainability Question

Can OpenAI keep this up? There are reasons to be wary. The easy wins in enterprise AI are mostly gone. The obvious early adopters, tech firms, financial services, media, are largely on board already. Growth from here means selling into more conservative industries with longer sales cycles and stricter compliance demands.

Commoditisation is the second worry. As open-weights models get better and cloud providers standardise hosting, the premium OpenAI can charge for API access will get squeezed. It is already up against price competition from Google, Anthropic, and a wave of cheap Chinese models.

Then there is the cost of running the business, which is brutal. Training a frontier model runs into the hundreds of millions of dollars per run, and serving enterprise customers at scale takes billions in GPU investment (OpenAI, capital and infrastructure context). The company has raised enormous sums to fund this, one figure put it at over $17 billion, but that badly understates the actual position: OpenAI reportedly raised around $122 billion in a single round in February 2026, with cumulative funding reported far higher. Either way, the appetite for capital is huge and ongoing.