Briefing

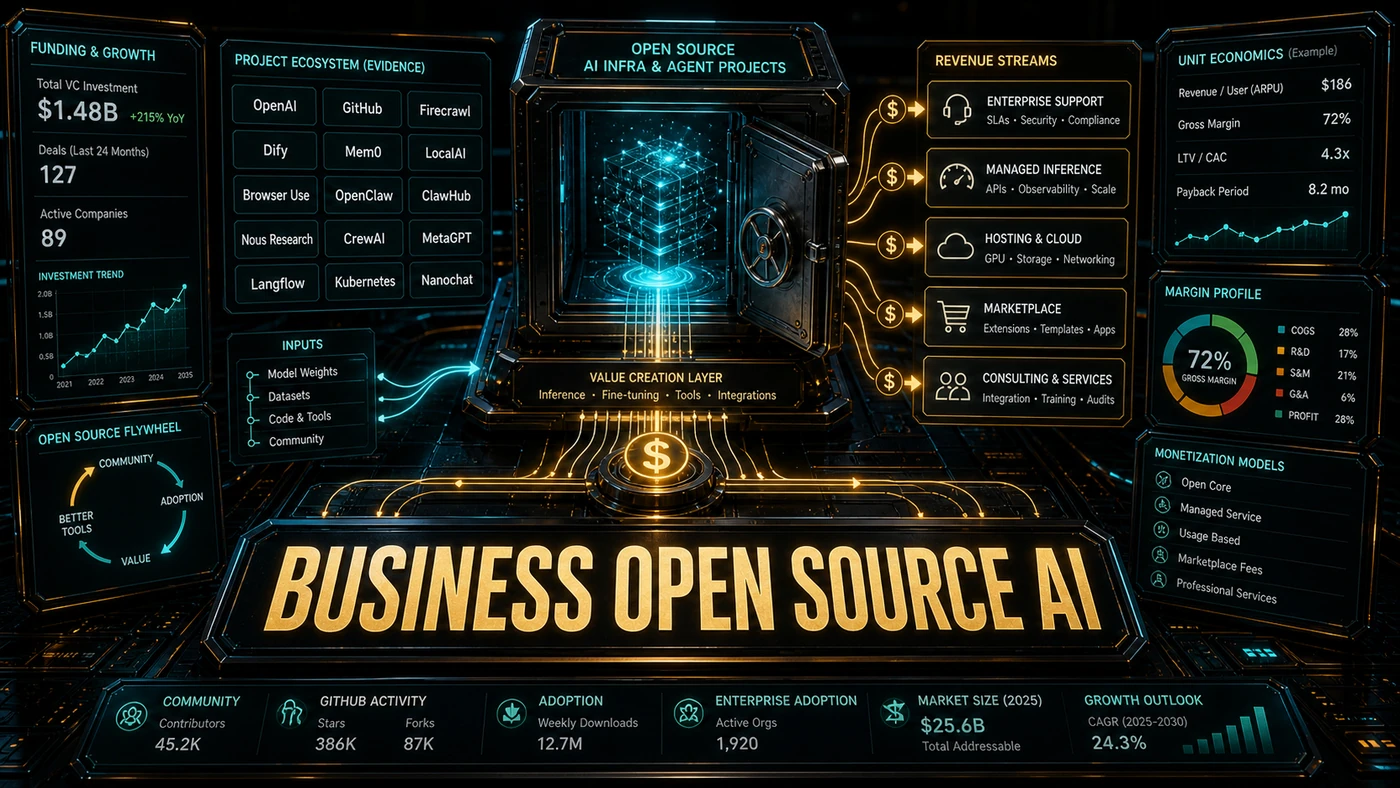

A few years ago, "open source AI" mostly meant a clever repo, a Discord server, and a maintainer working nights for free. That picture has changed. Some of these projects now have hundreds of thousands of GitHub stars, venture money in the bank, and paying enterprise customers. A handful are turning real revenue.

So if the code is free, where does the money come from? That's the question worth answering before you bet a workflow on any of these tools.

The short version: the popular project is rarely the product. The product is everything bolted around it, hosting, support, security, a place to deploy at scale. The repo earns the trust; the company sells the convenience. Below is how that plays out across the tools Australian teams are actually evaluating, who's funded, who isn't, and which claims floating around the space don't hold up.

The Open Source Business Model Spectrum

Pure Open Source: Some projects run with no commercial engine behind them at all. nanochat, Andrej Karpathy's end-to-end training pipeline, and awesome-claude-skills sit here. They're kept alive by individuals or small communities, paid for with sponsorships and goodwill. The point is reach and teaching, not income.

Open Core: The most common arrangement. The core is genuinely free and open, and the money sits in commercial extras for bigger users. Dify works this way, the self-hosted platform costs nothing, while cloud hosting, advanced features, and enterprise support are what you pay for (its paid Cloud tiers start at $59/mo).

Managed Services: Same software, but someone else runs it for you. Firecrawl offers a hosted crawling service next to its open codebase. Self-host for free, or pay so you don't have to think about it.

Consulting and Support: Enterprise clients pay for help getting it working, implementation, custom builds, production support. CrewAI and MetaGPT both have commercial offerings in this territory, though in practice both lean more toward an enterprise platform than pure consulting. CrewAI runs an Enterprise Cloud product, and DeepWisdom, the company behind MetaGPT, monetises through products like its Atoms coding tool.

Ecosystem Revenue: Marketplaces make money from distribution. ClawHub, the skill registry for OpenClaw agents, is reportedly looking at verified publisher programmes and enterprise registry services, though those revenue plans aren't confirmed.

Who's Raising Money

OpenClaw: This one needs a correction up front. The widely repeated story that OpenClaw raised a $100M-plus Series A in early 2026 doesn't appear to hold up, there's no evidence of such a round. What actually happened: the creator, Peter Steinberger (not "Cole Steinberger", as some write-ups have it), declined to build a company and joined OpenAI in February 2026, and OpenClaw continued as an independent open-source project. Treat any claim about an OpenClaw funding round at a $100M valuation as unconfirmed.

Mem0: The funding here is real. Mem0 raised $24M (Seed plus a Series A led by Basis Set Ventures) to build out its managed memory service. The bet is simple: every production agent needs memory, and Mem0 wants to be the default layer that provides it. AWS picked it as the memory provider for its Agent SDK, which tells you the thesis has buyers.

Firecrawl: Firecrawl raised a $14.5M Series A in August 2025, led by Nexus Venture Partners, and serves more than 350,000 developers. Its annual revenue is reportedly in the millions, though that figure isn't publicly confirmed. Growth is coming from agent developers who need dependable web access.

Langflow: Worth flagging the ownership here, because it changes the picture. Langflow is a popular open-source visual builder, but it isn't an independent company. It's owned by DataStax, which IBM agreed to acquire in 2025 and folded into its watsonx portfolio. The visual builder does lower the barrier for non-technical users, but claims of standalone Fortune 500 licensing revenue are unverified, the monetisation now runs through IBM/DataStax.

Nous Research: Another correction. Nous Research is often described as a non-profit living on grants and donations. It isn't. It's a VC-backed startup that has raised around $70M, including a $50M round led by Paradigm. It champions open-source AI, but it does so on a commercial-investor footing, not a charitable one.

Who's Not (Yet)

nanochat: Karpathy's educational project has no monetisation, and that's by design. The value is in teaching and the community around it, not in revenue.

Browser-use: This is frequently listed as pure open source with no commercial backing, but that's wrong. Browser Use raised $17M in seed funding (led by Felicis, out of Y Combinator's W2025 batch). It's open source, but it's funded.

LocalAI: A genuinely community-driven local-inference project. It appears to have no formal company structure behind it, though that detail isn't independently confirmed. Its pull is utility, not profit.

The Sustainability Challenge

The old open-source funding problem hasn't gone away. Popular projects with no revenue model run on volunteer time, and volunteer time runs out, that's how you get burnout and maintenance gaps. The risk isn't theoretical. In September 2025, a major npm supply-chain attack compromised 18 widely used packages (including debug and chalk, with roughly 2.6 billion weekly downloads between them) via phishing, followed by the self-replicating "Shai-Hulud" worm that hit hundreds more packages and stole cloud tokens. Incidents like that put the funding question back on the table.

A few funding routes have settled into place by 2026:

- [GitHub Sponsors](https://github.com/sponsors): Direct funding from users to maintainers

- Open Collective: Transparent funding for community projects

- Corporate Sponsorships: Companies paying to keep projects they rely on alive

- Foundations: The Linux Foundation, the Apache Software Foundation, and newer AI-specific foundations providing governance and money

The Enterprise Opportunity

The serious revenue is in enterprise adoption. Companies spending millions on AI infrastructure want support guarantees, security audits, and professional services, and they'll pay for them. Open-source projects that can offer that layer while keeping the core free are the ones capturing meaningful revenue.

It's the same pattern that played out before: Linux had Red Hat, Hadoop had Cloudera, Kubernetes had the cloud providers. The open-source project becomes the standard everyone uses, and the commercial business sells the things enterprises can't or won't do themselves.

Looking Ahead

This is still early, and the shape of it is likely to keep shifting. A few things look probable:

- Consolidation, as successful projects formalise into companies

- New funding models built specifically for open-source AI

- More corporate sponsorship as businesses lean harder on these tools

- Regulatory pressure to fund critical infrastructure properly

For teams choosing tools, the practical takeaway is reassuring: most of the projects you'd actually depend on are funded and maintained, not held together by one exhausted volunteer. Open-source AI isn't charity. It's a working business model, one where free software and paid services prop each other up, and everyone gets something out of it.