Analysis

The most-used AI tool on the planet probably isn't the one you'd guess. It isn't ChatGPT, and it isn't a search engine. It's the coding assistant that quietly sits inside a developer's editor and finishes their work as they type.

If you run a business, this matters even if nobody on your team writes code. The tools that build your software are getting cheaper to operate, faster to ship with, and harder for any one vendor to own. That changes who you buy from, how much you pay, and how quickly your suppliers can turn an idea into a working feature.

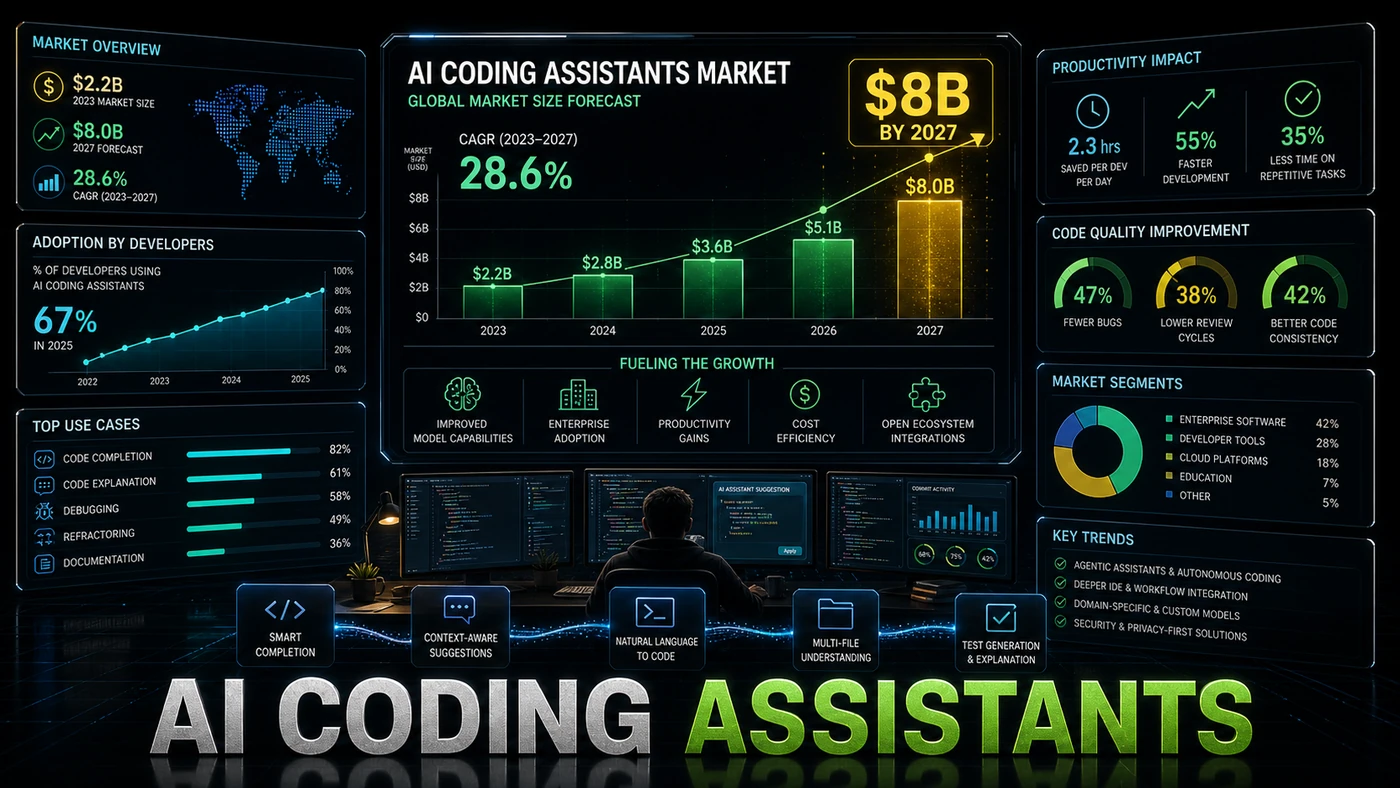

Here's the short version of the story: a market that was barely a rounding error two years ago is now worth billions, and the big platform owners (Microsoft, Google, Amazon, Apple) are racing to fold this capability into products you already use. The numbers below come with caveats, and we'll flag them as we go. But the direction is not in dispute.

The Adoption Drivers

A few things are behind the jump. The first is that the models got a lot better. Two years ago, coding assistants were glorified autocomplete: handy for finishing a line, occasionally useful on a small function, and wrong often enough that you couldn't trust them on anything hard. The newer models are a different animal. Tools built on Claude Opus 4.8, which scores 69.2% on the SWE-bench Pro benchmark (SWE-bench Pro Leaderboard, morphllm), Kimi K2.7-Code, and GPT-5.5 at 58.6% on the same benchmark (Introducing GPT-5.5, OpenAI) can write whole functions from a plain description, chase a bug across several files, and walk you through legacy code the way a senior engineer would. Worth noting: Kimi K2.7-Code's own published SWE-bench Pro figure is 58.6%, not the 64.8% sometimes quoted (Kimi K2.7-Code benchmarks, digitalapplied), and all three scores are vendor-reported rather than independently audited, so treat them as a rough capability signal, not gospel.

The second driver is that enterprise buyers have moved from dabbling to committing. Back in 2024, most of the usage came from individual developers or small teams paying out of pocket. By 2026, a reported majority of large enterprises have rolled these tools out across whole organisations rather than leaving it to individuals. (The widely cited "over 60% of Fortune 500 with organisation-wide deployments" figure isn't directly confirmed; related numbers exist, such as Cursor's claim that 67% of the Fortune 500 use it, but they measure slightly different things, per Sacra.) Either way, the purchase decision has shifted from a developer expensing a $20-a-month subscription to a CTO signing a six-figure annual contract.

The third is how deep the integration now runs. Early assistants lived in a separate window. The current crop sit inside the editor, the code review process, the build pipeline, and the documentation. That's what turns them from a nice-to-have into something a team would feel the loss of. A developer with an integrated assistant is measurably faster than one without.

The Key Players

GitHub Copilot, running on OpenAI models, is still out front with an estimated 45% of the market, though most 2026 sources land closer to 42% (GitHub Copilot Statistics 2026, getpanto). Microsoft's distribution is the reason: GitHub's 100 million-plus developers and VS Code's dominant share of editors give it a head start rivals find hard to close (GitHub Copilot Statistics 2026, getpanto). Copilot's annual revenue is often quoted at $2.5-3.0 billion, but that figure blends products together; analyst estimates put GitHub Copilot itself at around $1 billion in annual recurring revenue, with the larger number covering all of Microsoft's Copilot lines (GitHub Copilot Statistics 2026, getpanto).

Cursor, the AI-native editor, has become the strongest challenger. Estimates put it near 18% of the market, and its pitch is deeper AI integration, support for several model providers including Claude, GPT, and Gemini, and an experience built around AI assistance from the start (Sacra). On funding, be careful with the numbers floating around: reporting from April 2026 had Cursor's parent, Anysphere, in talks to raise $2 billion-plus at a valuation near $50 billion, not the $200 million at a $2.6 billion valuation that sometimes gets cited (Cursor in talks to raise $2B+ at $50B valuation, TechCrunch). The $2.6 billion figure was an older Series B valuation from December 2024.

After that the picture gets murkier. Sourcegraph Cody and the tool formerly known as Codeium, now Windsurf, are usually placed third and fourth, with rough shares of around 10% and 8%, though those percentages aren't backed by a clear source. Their framing is also dated: Sourcegraph moved Cody to enterprise-only in July 2025, and Codeium rebranded to Windsurf the same year. Both have leaned into enterprise needs: codebase-wide search, security and compliance controls, and fitting into existing toolchains.

The Market Structure Shift

The biggest change isn't who's winning today. It's that the platform owners are building this capability in by default. Google has put AI coding help directly into Android Studio and its cloud IDEs through Gemini Code Assist (ts2.tech). Amazon has folded its assistant deeper into AWS, now under the Amazon Q Developer name (the old "CodeWhisperer" branding was retired back in April 2024). And Apple has added AI coding features to Xcode, opening its tooling to MLX and open-source models at WWDC 2026 (Apple Outlines Major AI and Developer Tool Updates, MacRumors; the MLX framework is open source).

That's a problem for the standalone vendors. If every editor and platform ships a capable assistant for free, the market for buying one separately shrinks to teams with needs the defaults can't meet. The standalone tools have two options: match the platforms on integration, or pull ahead on capabilities the platform owners can't easily copy.